The point of trade agreements, above all, is to establish clear rules for cross-border commerce, so businesses can make sensible decisions about importing, exporting, and investing. One year into Donald Trump’s second presidency and that rationale is pretty much out the window when it comes to trade relations with the United States. The U.S. seems to have no compunction about ignoring agreements to which it is a party. This has major implications for value chains.

Diplomacy is a stop/start process, and no trade agreement is perfect. But agreements mean little if there is scant likelihood of compliance. Canada and Mexico were hit with 25% U.S. tariffs in 2025 in blatant disregard of the sweeping 2019 trade agreement between the three countries — never mind that negotiations to revise that agreement were already on the calendar for 2026. Colombia and the United States agreed to phase out tariffs on each other’s goods in 2012, but Colombia nonetheless got hit by a 10% tariff on most imports last April. The United Kingdom raced to get in the President’s good graces by striking a vague “Economic Prosperity Deal” in May 2025, but in mid-January Trump threatened it with additional tariffs if it did not support his demand that Denmark yield control of Greenland to the United States. Similarly, the European Union, Japan, South Korea, and other trading partners have found that their painstakingly bargained trade agreements with the United States are not binding.

While the U.S. Supreme Court may soon reject the claim that an “emergency” allows the president to impose tariffs as he desires, It is notable that neither major political party has had much to say about the Administration’s disrespect for U.S. trade agreements. This bipartisan indifference suggests that U.S. adherence to its commitments may remain uncertain even after Trump leaves office.

For more than a decade, many firms that once sourced mainly from China have quietly opened factories or sought suppliers in other countries. That approach, known as “China plus one,” may no longer be sufficient. With the United States now sanctioning numerous trading partners as it sees fit, managing value-chain risk may require multiple options in case a second-choice supplier country falls from Washington’s good graces. “China plus two or three” is likely to be an expensive strategy, making it harder to gain economies of scale, but it may be wiser than assuming that U.S. trade agreements will be adhered to.

Category: Uncategorized

-

China Plus Two or Three

-

The Government’s Tariff Bill

U.S. tariffs supposedly generated a record $31 billion in revenue during the month of August. According to a breathless report from Fox News, “The US could collect as much tariff revenue in just four months to five months as it did over the entire previous year.” But while those numbers may prove accurate, they represent only one side of the federal government’s ledger. There’s hasn’t been much attention to the fact that with the tariffs Washington is effectively taxing itself.

President Trump has set a tariff rate of 50% on steel, copper, and aluminum imports from most countries, excluding Great Britain. He has also imposed a 50% rate on the steel or aluminum content in 407 different products, from truck trailers to barbecue forks with wood handles. Those tariffs don’t just affect imports. By making foreign products more expensive, they make it easier for domestic producers to jack up prices; were that not the case, the tariffs would serve no purpose.

And who buys that domestic metal? Much of it ends up in goods purchased by Uncle Sam (fighter planes, postal delivery trucks) or by state and local governments using federal as well as state money (girders for highway bridges, pipes for water systems). With the tariffs in effect, governments buy less with each dollar they spend on such things.

Steep tariffs on pharmaceuticals are supposedly impending. The United States and the European Union have agreed that European drugs will face a 15% U.S. tariff, and Trump has threatened tariffs of up to 250% on drugs from other countries. Since the Washington pays 59% of the cost of outpatient prescription drugs and the states pay another 5% to 10%, governments will bear most of the burden of higher prices.

These tariffs are not affected by the recent court decision blocking many of the tariffs Trump has proposed. They could remain in place indefinitely. And as long as they do, U.S. taxpayers will pay far more than they should for the goods their tax dollars buy.

-

Dominance

Donald Trump is into dominance. In a series of orders since he started his second term last January, he has proclaimed his intention to restore America’s maritime dominance and its energy dominance, to make the United States dominant in cryptocurrency and artificial intelligence, and to maintain the dollar as the world’s dominant currency. And that’s not all. “America’s destiny is to dominate every industry,” he told an audience in Pennsylvania on July 15.

In recent days, Trump reasserted his belief in U.S. dominance by announcing steep tariffs on many countries. His quest for dominance goes beyond eliminating bilateral trade deficits. He has placed tariffs on imports from Canada, supposedly because it allows fentanyl to cross the border into the United States; and on Brazil (with which the United States has a trade surplus) to punish it for prosecuting a former president for plotting the violent overthrow of the government; and on India, supposedly because it purchases oil and military equipment from Russia. Tariffs, he clearly believes, are a useful cudgel to force other governments to conform to his desires.

In the short term, large bilateral trade deficits have made it difficult for trading partners to retaliate when Trump nullifies longstanding trade agreements and announces new import barriers. In the longer term, though, such policies threaten the United States’ central place in the world economy. U.S. disinterest in expanding international trade and negotiating multilateral agreements is not shared by most other countries, which are busily signing trade packs that do not include the United States. Talk about creating a substitute for the World Trade Organization without U.S. involvement is widespread.

Already, traders are responding to America’s anti-trade agenda by finding other partners. “Since this March, China-ASEAN export volumes are now double that of China-US, traditionally the most important route in container shipping,” Bloomberg reports. On August 5, the Bureau of Economic Analysis confirmed that while U.S. imports are declining, its exports are in decline as well. As America withdraws, other countries are moving forward, and U.S. dominance is slowly falling away.

-

What Fred Smith Did

“Move fast and break things” is the mantra for those who start companies in the digital age. That wasn’t so easy for Fred Smith. Smith, who died on June 21, founded parcel giant Federal Express Corporation, now called FedEx. He is often credited with conceiving the hub-and-spoke system of package delivery. That is inaccurate; as best I can tell, the hub-and-spoke concept was developed by the predecessor to United Parcel Service in the 1910s. Smith’s great contribution was to demolish regulations that stifled innovation in transportation.

When Smith founded Federal Express, in 1971, U.S. air transportation was tightly controlled. Both passenger and all-cargo airlines had to prove to the Civil Aeronautics Board that public convenience and necessity justified any new route. Incumbent carriers usually sought to block any new service. Federal law, however, exempted very small planes from CAB’s economic regulations. That’s why Federal Express took off in 1973 with planes designed to carry nine passengers. By establishing a hub in Memphis — something that airlines flying larger planes could not do without CAB approval of each route — it initially moved documents and computer parts among 25 cities. Soon thereafter, the CAB exempted slightly larger planes from economic regulation, and Federal Express took full advantage. “Nobody at the Civil Aeronautics Board ever thought that somebody was going to use that change in the regulations to put a nationwide overnight air express system in place,” Smith told me when I spoke with him last year. “But that’s what permitted it.”

With business booming, Smith wanted to buy full-size jets. In 1975, the CAB refused approval. He descended on Washington, telling anyone who would listen how regulations were stifling a new type of air freight service. Debates over airline deregulation were just beginning, and when deregulating passenger service proved too complicated to accomplish in 1977, Congress approved a much simpler bill eliminating the CAB’s authority over air cargo. The Air Cargo Deregulation Act, now generally forgotten, made it practical to offer overnight delivery service nationwide.

Smith also ran up against the Interstate Commerce Commission, the agency that regulated surface transportation. The ICC allowed airlines to pick up and deliver air cargo only within 25 miles of an airport they served. When it proposed to expand that zone to 35 miles in 1979, more than 1,600 parties objected. Smith played a role once more as Congress deregulated trucking the following year, enabling Federal Express to pick up and deliver anywhere in the country.

The sweeping deregulation of transportation that Fred Smith helped achieve underlies the massive growth in international trade starting in the 1980s. Ironically, another key figure in globalization chose not to be part this story. Smith told me that he tried to recruit container shipping pioneer Malcom McLean as an early investor in Federal Express. “McLean turned me down,” Smith said, “but we had a nice relationship.”

-

Burner Phones

A year and a half ago, before a trip to China, I spoke with several people in Washington who know that country far better than I. They all gave me the same advice. My electronic devices would be examined by Chinese authorities the moment I set foot in the country, they warned. I should leave my electronics at home, they said, and take only a burner phone.

I recalled those conversations a few days ago at a meeting of the Maritime Research Alliance in Denmark. During my trip, I learned that the Copenhagen Business School, one of the country’s leading educational institutions, has advised its staff to bring only burner phones when visiting the United States. If they carry other devices, the university has warned, immigration authorities could inspect the contents and use them as an excuse to deny entry into the country.

This is frightening. And dangerous.

At the moment, the U.S. government seems very hostile to foreigners, supposedly in the interest of national security. “Visiting America is not an entitlement. It is a privilege extended to those who respect our laws and values,” Secretary of State Rubio insists.

This tough-at-the-border attitude is supposedly protecting national security. Over decades, however, nothing has protected America’s national security more than its openness. Around the world there has been a deep well of public sympathy for the United States. Its openness to diverse points of view is one reason people in other countries have sought to visit, study, and do business in the United States. By giving visitors reason to fear that they may be detained by an immigration officer for expressing views that may differ from Mr. Rubio’s or for having a suspect name in their contact books, the United States is doing nothing more than isolating itself from the world.

The story of the French scientist headed to a conference of space researchers who was turned back by immigration officers at Houston Intercontinental Airport is well known in Europe. Companies, including U.S.-based companies, are discouraging foreign executives from traveling there, especially if they are Muslim or Chinese. “Danes really used to admire the United States,” one Danish acquaintance told me. “Now, not so much.” That ought to worry us much more than a critical sentence on a visitor’s computer.

-

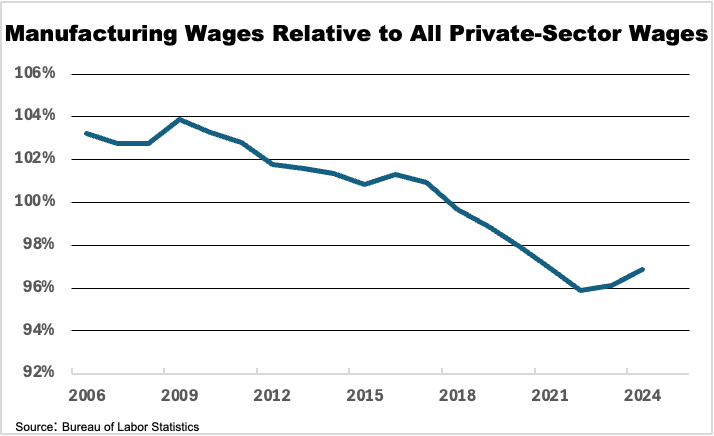

Factory Job

The Trump Administration is racing to discharge tens of thousands of federal workers in order to do away with government activities it dislikes. And what are those displaced workers to do? Treasury Secretary Scott Bessent offered an answer on April 7. “[W]e are shedding excess labor in the federal government,” he said, adding, “That will give us the labor that we need for the new manufacturing” which, he asserts, the Trump Administration’s higher tariffs will bring to the United States.

This advice fits neatly with persistent claims that manufacturers can’t find workers. Last year, the head of the National Association of Manufacturers claimed that there were 800,000 unfilled manufacturing jobs. That number is likely to grow if the Administration succeeds in reducing the number of immigrants in the United States.

This purported labor shortage is usually attributed to spoiled workers who avoid jobs that can be dirty and physically taxing. As one economist insists, “Young people, especially, are not interested in jobs in manufacturing.”

Count me as skeptical. In general, I think, workers are good at sniffing out the best opportunities. The reason many shun manufacturing jobs is that, on average, they are no longer good jobs. Manufacturing workers used to earn a premium relative to workers in other industries. Due in part to foreign competition, that premium has vanished. Many of the fringe benefits that union factory workers used to enjoy have vanished as well.

If theory, higher tariffs should help manufacturers earn greater profits from U.S. operations. But will higher profits mean better pay? It hasn’t worked out that way in the past: in primary metals, where steep tariffs protect the steel and aluminum industries, inflation-adjusted wages for production workers are five percent below their level in 2005. Does Mr. Bessent have a plan to ensure that any benefits of disrupting global supply chains are spread widely? If not, persuading displaced federal workers to staff newly built factories may be a hard sell.

-

Terminal Risk

Back in 2006, when he was considering a second run for president, Senator John Kerry visited the bank where I worked in search of support (and contributions). He spoke about the plans of Dubai Ports World to take over U.S. container terminals by acquiring the troubled British shipping group Peninsula & Oriental. Dubai Ports, now known as DP World, was (and still is) controlled by the Emirate of Dubai. Its ownership of container terminals, Kerry warned us, would make it easier for Arab terrorists to launch attacks in the United States.

Kerry was not alone. After it became clear that Congress would block the deal, Dubai Ports sold P&O’s U.S. operations to a U.S. owner. Those assets eventually came under the control of a company now known as Ports America, which still owns them. Ports America, despite its name, is largely Canadian owned. In a delicious irony, it has been led since 2022 by a chief executive who was formerly chief operating officer of DP World’s ports and terminals. No one seems to be exercised about potential links to terrorists.

The recent kerfluffle over the ownership of container terminals at both ends of the Panama Canal by CK Hutchison Holdings brought back memories of the Dubai Ports debate. Hutchison, based in Hong Kong, is a publicly traded company and was a pioneer in developing container terminals. After President Trump declared in his inaugural address that “China is operating the Panama Canal,” Hutchison’s management apparently determined that the time was right to shed most of its terminals and avoid becoming the target of China hawks in Washington — never mind that the notion that China could use the Hutchison terminals in Panama to block the canal seems a bit farfetched.

President Trump now asserts that the United States is “reclaiming the Panama Canal” by virtue of New York money manager BlackRock’s role in acquiring Hutchison’s terminals. But matters aren’t quite so simple.

If the transaction is completed, Mediterranean Shipping Company, the world’s largest container ship line, will take a significant stake in the terminals. MSC is owned by an Italian family and is based in Switzerland. Its finances are private.

Would its role in the terminals in Panama reduce the purported security risks of Chinese influence there? The Trump Administration itself may not think so. The Administration plans to impose “service fees” on arriving vessels operated by companies that own ships built in China, which the United States accuses of “targeting of the maritime, logistics, and shipbuilding sectors for dominance.” MSC likely has hundreds of Chinese-built vessels in its fleet of 900 container ships and would be among the largest targets of those U.S. sanctions. In today’s Washington, it’s not hard to imagine someone asserting that China could use its role in providing MSC with ships to influence the operation of the terminals in Panama. If you’re determined to identify risks, you’re likely to find some.

-

Forgetting Friendshoring

Remember friendshoring?

Back in the days of COVID-19, when manufacturers and retailers suddenly paid attention to supply-chain risks they had previously ignored, the notion that they could reduce risk by “reshoring” manufacturing from abroad to U.S. locations came into vogue. The concept has some obvious limitations: it doesn’t eliminate the risks of relying on a single source of critical inputs or finished products, and costs make it impractical to produce many things domestically. “Nearshoring” was advanced as an alternative: perhaps some production could be moved from Asia to lower-wage U.S. neighbors. “Friendshoring” emerged during the Biden Administration — former Treasury Secretary Janet Yellen is often credited for coining the term — as another option, the idea being that national security risks could be controlled by sourcing sensitive goods from countries that are aligned with U.S. interests as well as from the United States.

Since he took office on January 20, President Trump has taken or threatened unfriendly actions against some of those friends, including several countries — Panama, Colombia, Mexico, Canada — with which the United States has signed agreements to eliminate tariffs and other trade barriers. The announced tariffs on imports from China would also strike at many firms that draw on important inputs from China but are based in other friendly countries, such as Japan, South Korea, and Taiwan.

The Trump Administration hasn’t had much to say about friendshoring, but its actions, whatever their other purposes, undermine the rationale for it. Companies that shift important links in their supply chains to “friendly” countries can no longer assume unfettered access to the U.S. market. That uncertainty may be enough to convince some firms to leave their Asia-based supply chains intact: If moving supplier locations doesn’t lower the firm’s costs or reduce the risk that trade barriers will interrupt its supply chains, why should it bother?

The danger, of course, is that a decision that seems sensible for a firm may not be so sensible from a national security perspective. By being unfriendly toward friends, the United States may be increasing the very risks in critical supply chains that it has sought to minimize.

-

What’s at Stake in the Longshore Negotiations

The International Longshoremen’s Association, whose members operate the container terminals along the Atlantic and Gulf coasts, threatens to strike on January 15 unless employers back away from introducing more automation on the docks. The union can’t simply hold back the tide: it needs to ensure that the cost of using ports that have ILA contracts doesn’t divert cargo to Pacific ports, where the International Longshore and Warehouse Union — a union perpetually at odds with the ILA — holds sway. But whatever concessions ILA president Harold Daggett wins, he may have already accomplished something more important in the long run, turning his notoriously fractious union into a more unified one.

So far as I’m aware, no thorough history of the ILA has ever been written. Here’s a capsule version. The union originated in the Great Lakes in the late 1800s, but it has been centered on New York since the early 1900s. For most of that time, it has been rent by internal quarrels. In 1937, its West Coast locals, deeming the ILA insufficiently class-conscious, split off to form the ILWU. Headquarters had only sporadic control over locals at other ports, including Brooklyn, where the predominantly Italian-American leadership openly ignored dictates from the Irish-Americans in Manhattan. Through the 1960s, the ILA battled constantly with other unions, most notably the Teamsters, for control of vessel loading and unloading (usually with success) and of warehousing and truck loading on the waterfront (usually unsuccessfully). The ILA’s ties to organized crime made it a perpetual subject of investigation, leading the American Federation of Labor to try unsuccessfully to replace it with a new union in 1953. ILA locals in other ports often treated directives from headquarters as optional. As the journalist Murray Kempton once jibed, the ILA was “the only anarchist union.”

Through all of this, individual dockers had to go begging for work each morning, hoping that their connections to a pier boss, sometimes lubricated with kickbacks, would get them a day’s pay. This began to change during the 1960s, as container ships began calling at new terminals in New Jersey. In 1965, the ILA agreed to accept containerization in return for the pledge of a guaranteed income for dockers who lost work due to the new technology, almost all of whom were in Manhattan and Brooklyn. The result was a much smaller but far better paid workforce.

The funding for the guaranteed income came from a tax on each container entering the Port of New York. This tax encouraged the shift of traffic to the South, where Savannah, Houston, Hampton Roads, and Charleston became major container ports. All these ports are in states where contracts cannot require workers to join a union and where political support for unions is weak. To protect the union’s position, some local ILA officers in those places have made side deals with port employers that the parent union has had little choice but to accept.

Daggett’s attack on automation seems to have overcome these centrifugal forces, winning support among ILA locals from Maine to Texas. This is no minor accomplishment. A successful negotiation would likely bolster the position of the central leadership to an extent the union has never known. That could well make the ILA an even tougher bargaining partner for the shipping industry in the years ahead.

-

About That Manufacturing Renaissance

The Biden Administration asserts there’s a “manufacturing renaissance” underway in the United States. Before it, the Trump administration claimed much the same. The federal government has certainly handed out a good deal of money to support manufacturing, in addition to aiding it with tariffs put in place by both Trump and Biden. But while manufacturing capacity, as measured by the Federal Reserve Board, has increased about 2.3 percent since Biden took office in 2021, labor productivity in manufacturing — basically, output per work hour — is down, according to figures released in early December. Total factor productivity, a measure of how industries improve technology and production processes to squeeze more output from a given quantity of inputs, fell in manufacturing in 2023 even as it rose in most other U.S. industries. These facts help explain why the Fed’s Industrial Production Index has been flat since the Obama years, save for a dip during the COVID-19 pandemic.

How does this square with the boom in factory construction and the many newspaper articles about new factories reviving down-at-the-heels communities? What seems to be going on is less a manufacturing renaissance than a restructuring. According to the Census Bureau, the computer, electronic, and electrical manufacturing sector has accounted for well over half of manufacturers’ construction spending this year, and construction in the transportation equipment sector is also strong. Meanwhile, construction in other manufacturing sectors has barely grown or even declined after accounting for inflation.

This is relevant to the much-discussed “reshoring” of manufacturing. To the extent that “reshoring” is underway, it seems to be concentrated in a handful of sectors, notably semiconductors, electric vehicle batteries, pharmaceuticals, and medical equipment. There are few signs of U.S.-made goods supplanting imports of industrial machinery, plastics and rubber products, synthetic fibers, paper, textiles, and any number of other products. Despite all the government support and the talk of tariffs, many manufacturers don’t seem to see the future in the United States.